Key Takeaways

Choosing the right life insurance requires adequate coverage assessment, early purchase, full disclosure of information, careful product selection, and thorough review of policy terms. Evaluate insurers holistically and avoid depending solely on employer coverage to ensure long-term financial protection for your dependents.

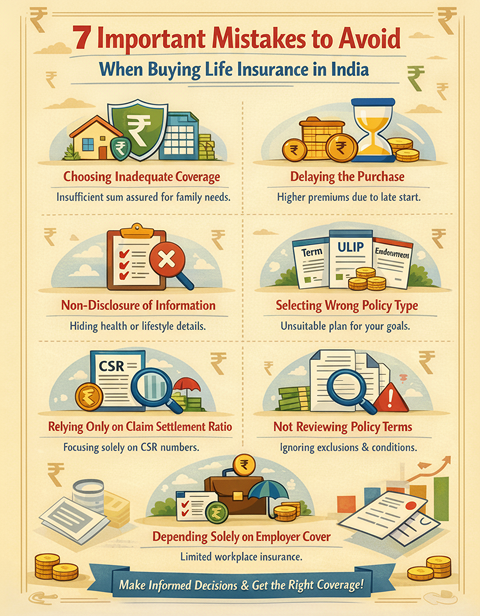

Life insurance plays a significant role in financial protection planning. However, purchasing a policy without understanding the coverage requirements, policy terms, and all necessary disclosure obligations may lead to complications in the future while filing the claim. So, today we are going to discuss seven important considerations to help individuals make informed decisions.

1. Choosing Inadequate Coverage

One common mistake people make while selecting a sum assured is they consider only affordability, but this may cause an inadequate protection of their dependents.

Factors to evaluate include:

- Annual household expenses

- Outstanding liabilities (home loan, personal loan, etc.)

- Children’s education and future goals

- Inflation impact over time

2. Delaying the Purchase

Life insurance premiums are generally low at the early ages, as they are influenced by health condition, lifestyle, and underwriting assessment. Hence, early purchase may result in relatively lower premiums, subject to medical evaluation and insurer approval.

3. Non-Disclosure of Material Information

Providing incomplete or inaccurate information regarding health, lifestyle, occupation, or medical history is one of the common mistakes that may impact your claim admissibility.

Policy applicants should:

- Disclose all material facts accurately.

- Carefully review the proposal form before signing.

- Retain copies of submitted documents.

Claims are assessed as per policy terms and disclosures made at the time of proposal.

4. Selecting an Unsuitable Product Type

Different life insurance products serve different purposes. So, it is very crucial that you select a suitable life insurance product type that aligns with your specific goal:

- Term Insurance Plans: Pure risk protection with no maturity benefit (unless specified).

- Endowment Plans: Combine insurance with savings features.

- Unit Linked Insurance Plans (ULIPs): The Ulip Policy provides insurance along with market-linked investment components.

ULIPs are subject to market risks, and investment returns are not guaranteed. Policy benefits depend on fund performance and applicable charges. Product selection should align with your financial goals, risk appetite, and time horizon.

5. Relying Only on Claim Settlement Ratio

Claim Settlement Ratio (CSR), published annually by IRDAI in its Annual Report, is one indicator among many. Policyholders are encouraged to evaluate insurers based on:

- Solvency ratio

- Product features and exclusions

- Premium affordability

- Service track record

- Policy terms and conditions

A holistic evaluation aids informed decision-making.

6. Not Reviewing Policy Terms and Conditions

Before purchasing, applicants should carefully review:

- Exclusions

- Waiting periods

- Grace period provisions

- Surrender and revival conditions

- Claim procedures

- Free-look cancellation period (as per IRDAI guidelines)

Understanding the policy terms helps in avoiding future misunderstandings.

7. Depending Solely on Employer-Provided Coverage

A group insurance provided by your employer may not be portable upon change of employment, or it may not offer adequate coverage as per your requirements. Hence, a separate individual policy can help to maintain continuity of coverage, subject to insurer underwriting.

How Inbest Assists Clients

Inbest is a registered insurance broker that can assist its clients by:

- Assessing their protection needs

- Comparing policy features across insurers

- Explaining product terms, exclusions, and conditions

- Facilitating documentation and proposal submission

- Assisting during claim coordination as per insurer processes

Inbest acts as an intermediary and does not underwrite risk. The insurance contract is between the insurer and the policyholder, and policy issuance is subject to underwriting approval.

Final Note

Life insurance decisions should be based on informed evaluation of policy features, risks, and individual financial needs. Prospective policyholders are advised to read the sales brochure and policy document carefully before concluding a purchase decision. If you are also planning to take a life insurance plan, then evaluate all the above-mentioned important mistakes that you need to avoid in order to obtain desired coverage and reduce the likelihood of claim-related issues.

Disclaimer

Insurance is the subject matter of solicitation. The information provided is for educational purposes only. Policy benefits are subject to the terms and conditions of the insurer. Inbest acts as a licensed insurance direct broker (Registration No. 831). Readers are advised to review policy documents carefully before purchase.