Key Takeaways

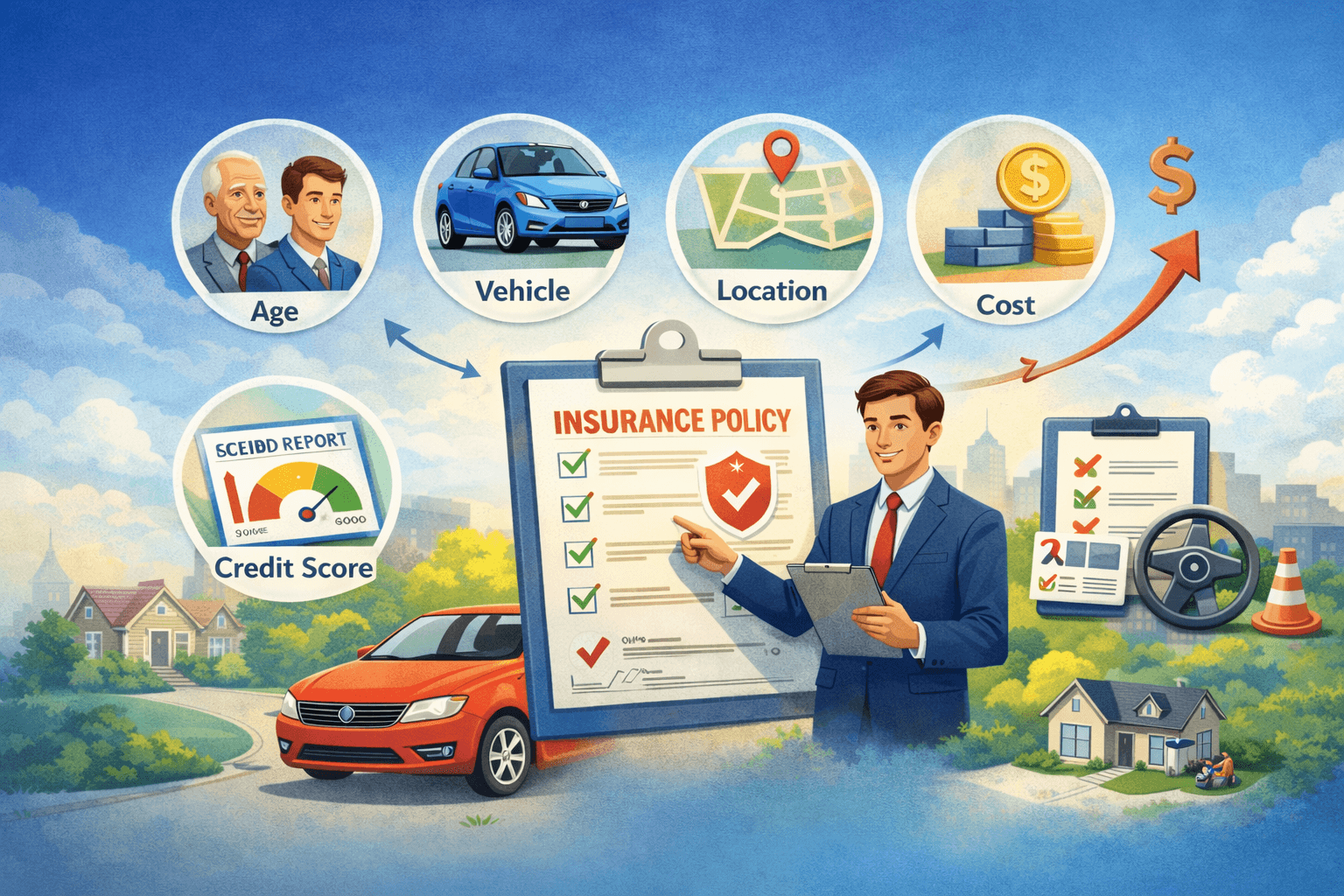

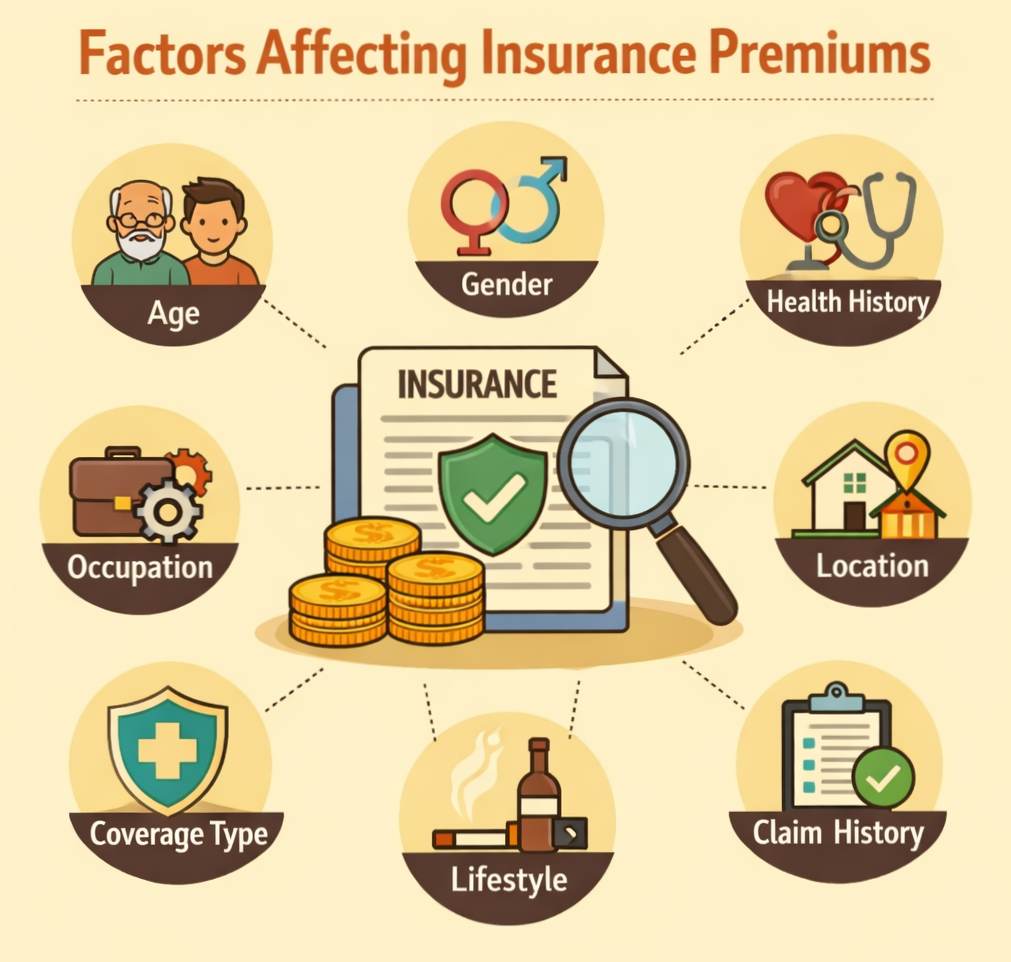

Insurance premiums are determined through risk assessment based on factors such as age, gender, health history, lifestyle, occupation, location, coverage type, and claim history. Understanding these factors helps individuals in choosing suitable insurance coverage while managing premium costs effectively and responsibly.

An insurance premium is the amount paid by a policyholder to an insurer in exchange for coverage under a policy. The premium is determined after assessing several risk-related factors that help insurers estimate the probability of a claim. These evaluations ensure that the premium remains fair, transparent, and proportionate to the level of risk associated with the policy.

Below are some of the common factors that may influence the insurance premium amount.

Age

Age is one of the most significant factors considered while determining insurance premiums, particularly in life and health insurance policies. Generally, younger individuals are considered to have a lower probability of making claims and may therefore be offered comparatively lower premiums. As individuals grow older, the likelihood of health-related risks may increase, which can lead to higher premiums.

Gender

Gender may also be considered in certain insurance products where actuarial data supports such differentiation. For example, statistical data often indicates that women have a longer life expectancy compared to men. In some life insurance products, this difference may result in relatively lower premiums for women.

Family Medical History

Family health history may be evaluated during the underwriting process, especially for health and life insurance policies. If any hereditary medical conditions, such as heart disease, diabetes, or certain cancers, are prevalent in the family, insurers may consider this information, and this may influence the premium amount or policy terms.

Type of Insurance Coverage

The type and extent of coverage selected by the policyholder also play a significant role in determining the premium. Policies that offer broader coverage or include additional riders and benefits may have higher premiums compared to basic policies with limited protection.

For instance, riders such as critical illness cover, maternity benefits, or accidental disability cover can enhance the protection provided by a policy, but they may also increase the overall premium.

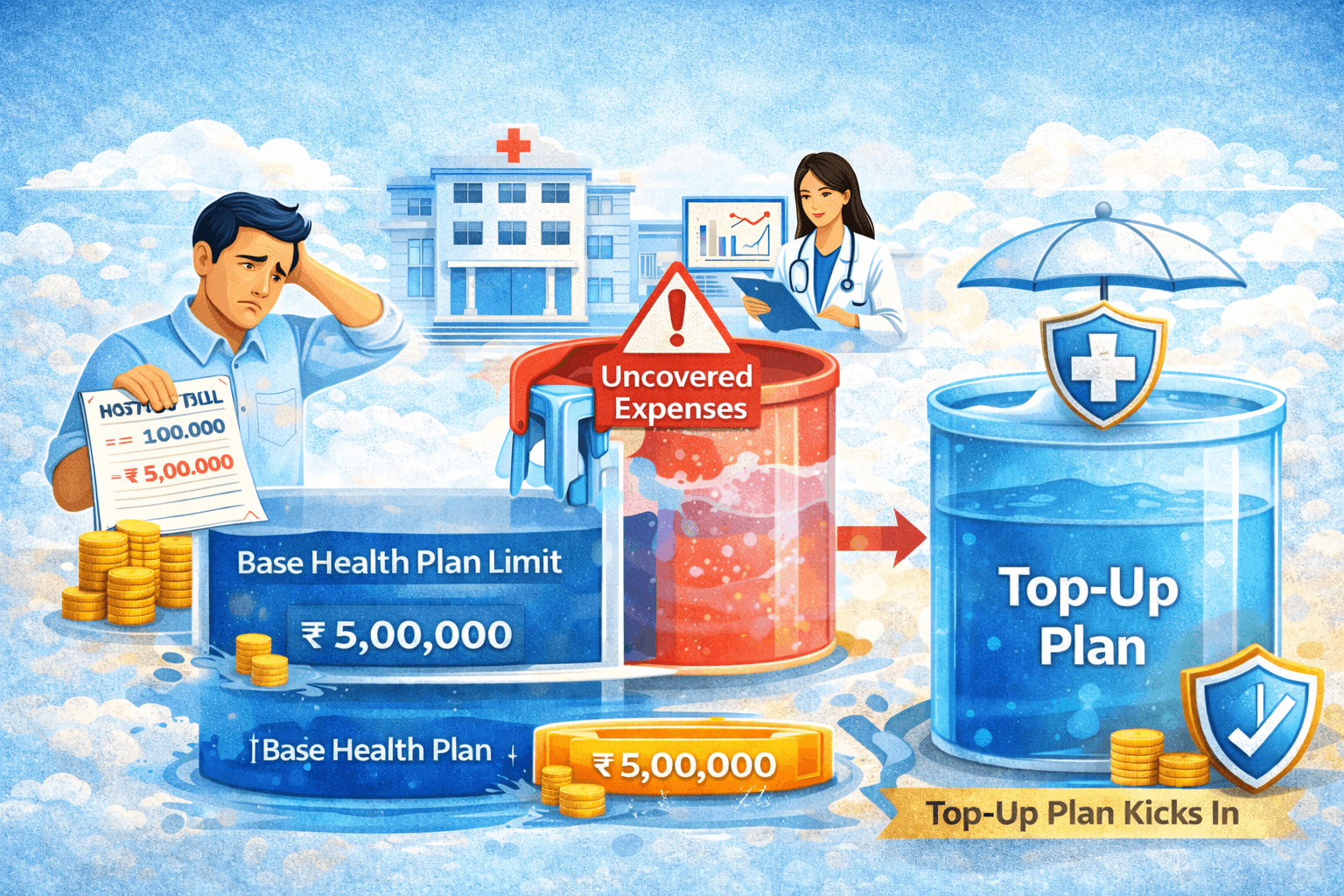

Sum Insured (Coverage Amount)

The sum insured, which represents the maximum amount payable by the insurer in the event of a valid claim, directly influences the premium amount. A higher sum insured generally leads to a higher premium because the insurer assumes greater financial liability. Conversely, selecting a lower coverage amount may result in a lower premium.

Health Condition and Lifestyle

The applicant’s current health condition is an important factor in the underwriting process. Individuals with pre-existing medical conditions may be charged higher premiums or may be offered coverage with specific conditions.

Lifestyle habits may also be considered. Factors such as smoking, alcohol consumption, or participation in hazardous activities may increase the perceived risk and could influence the premium amount.

Occupation

An individual’s occupation can also impact insurance premiums. Professions that involve higher levels of physical risk, such as construction work, mining, or certain industrial jobs, may lead to higher premiums compared to occupations that involve relatively lower risk.

Location

The geographical location of the insured person or property may also influence premium calculations. For example, properties located in areas prone to natural disasters or regions with higher crime rates may attract higher premiums due to increased risk exposure.

Insurance and Claim History

Insurers may also review the applicant’s previous insurance and claims history. Individuals who have made multiple claims in the past may be considered to have a higher risk profile, which may influence the premium or the terms offered under the policy.

Underwriting and Rating Factors

During the underwriting process, insurers gather relevant information about the applicant and evaluate multiple rating factors such as age, location, coverage limits, policy tenure, and deductibles. Each factor contributes to the overall risk assessment, which ultimately determines the premium amount.

Conclusion

Insurance premiums are determined through a systematic evaluation of several risk-related factors. These calculations are based on actuarial data and underwriting principles while adhering to regulatory guidelines in India. Understanding the factors that influence insurance premiums can help you make more informed decisions while selecting insurance coverage that aligns with your financial needs and risk profile.

Disclaimer: Insurance is the subject matter of solicitation. The information provided is for educational purposes only. Policy benefits are subject to the terms and conditions of the insurer. Inbest acts as a licensed insurance direct broker (Registration No. 831). Readers are advised to review policy documents carefully before purchase.